The real estate world is undergoing a digital transformation—and it’s being driven by blockchain technology. Traditionally, investing in real estate required significant capital, intermediaries like banks and agents, and a great deal of time. But with real estate tokenization, the game is changing dramatically. Now, owning a piece of property could be as simple as owning a digital token.

What Is Real Estate Tokenization?

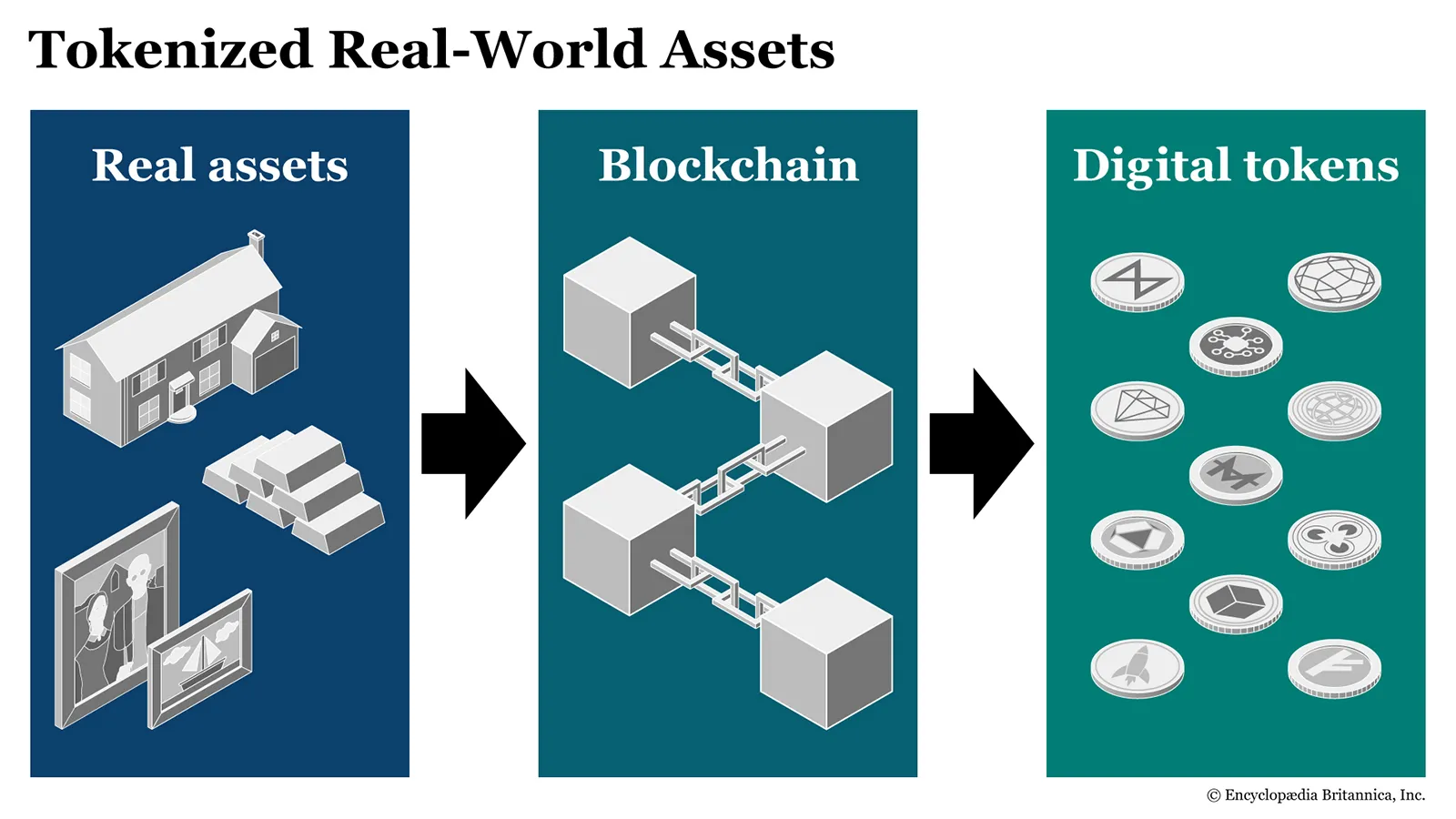

Real estate tokenization is the process of converting ownership of a physical property into digital tokens on a blockchain. These tokens can represent fractional ownership in residential, commercial, or industrial real estate. Through this method, assets are divided into small, tradable units, opening the door for smaller investors to participate in markets that were once inaccessible.

These tokens can be issued as NFTs (non-fungible tokens) for unique properties or as fungible tokens when fractional shares are involved. The ownership, transfer, and transaction history of these tokens are recorded immutably on the blockchain, providing transparency and reducing fraud.

Why Is This Important?

-

Accessibility & Inclusion

Tokenization lowers the entry barrier by allowing investors to purchase fractions of real estate, meaning you no longer need $100,000+ to get started. With as little as a few hundred dollars, investors can now own a portion of a property. -

Liquidity

Real estate has traditionally been illiquid—you can’t just sell your house in a day. But tokenized real estate can be traded on secondary markets, giving investors a way to buy and sell their positions more freely and efficiently. -

Efficiency & Speed

Smart contracts eliminate many of the middlemen typically involved in real estate transactions—like escrow agents, notaries, and banks—reducing fees and processing times. -

Transparency & Security

Blockchain provides a secure and auditable record of all ownership transactions, making fraud and title disputes far less likely. Everything from rental income distribution to capital gains is recorded and automated.

Who’s Getting Involved?

Major players are already entering the space. In the U.S., real estate tokenization is being pioneered by platforms like RealT and SolidBlock. Internationally, Dubai recently saw a tokenized villa sell out in under 5 minutes, thanks to Prypco Mint—demonstrating both the speed and appetite for this investment model.

Meanwhile, ESG‑aligned blockchain projects such as Trrue (Ireland) are aiming to tokenize real-world assets including sustainable real estate, green bonds, and infrastructure. These initiatives combine the environmental, social, and governance (ESG) movement with digital ownership, pushing green investing to the blockchain frontier.

Millennials and Gen Z: The New Digital Landlords

Younger generations, already familiar with digital wallets and NFTs, are becoming key participants in this ecosystem. Tokenized real estate offers them the benefits of property investment—income, appreciation, diversification—without the overwhelming costs or bureaucracy.

This demographic shift is driving innovation in platforms that are mobile-friendly, ESG-aware, and digitally native. With climate consciousness on the rise, many of these platforms are also prioritizing energy-efficient properties and green building certifications.

The Future: Sustainable Digital Cities?

Looking ahead, we may see entire smart cities or eco-communities financed and operated through tokenized systems. Investors could directly support sustainable housing, renewable energy projects, or climate-resilient developments through token purchases. These digital systems would ensure that capital flows to projects that align with environmental and social values.

Real estate tokenization isn’t just a tech trend—it’s a paradigm shift. It democratizes access, streamlines processes, and aligns seamlessly with the demands of a digital, sustainable future. Whether you’re a millennial looking to break into property ownership or an institutional investor seeking ESG-aligned opportunities, this is a space worth watching.