As environmental challenges become more pressing, innovative technologies are emerging to address these global concerns. Blockchain, a decentralized ledger system best known for its role in cryptocurrencies, is proving to be a powerful tool for advancing environmental sustainability. The United Nations Environment Programme (UNEP) highlights how blockchain applications can promote greener practices through supply chain monitoring, decentralized energy systems, and innovative financial instruments.

1. Enhancing Supply Chain Transparency

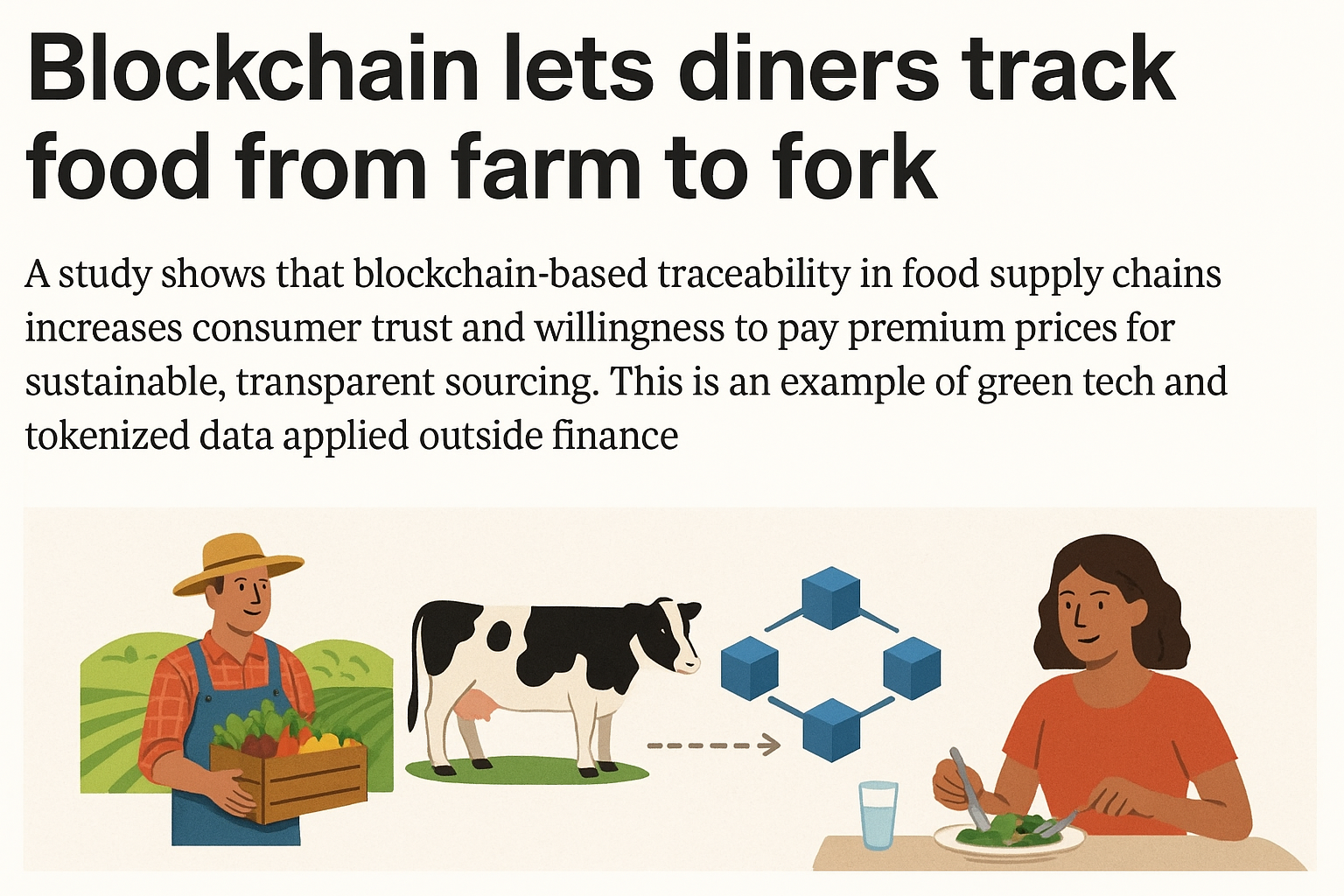

Supply chains often involve complex networks where inefficiencies and unethical practices, such as illegal logging or overfishing, can go unnoticed. Blockchain offers a transparent and tamper-proof way to track every stage of the supply chain. By integrating blockchain, companies can:

- Monitor the origin of raw materials: Verifying sustainable sourcing for products like coffee, palm oil, and seafood.

- Reduce waste: Identifying inefficiencies and streamlining logistics to minimize environmental impact.

- Build consumer trust: Providing customers with verifiable data about a product’s journey from source to shelf.

For instance, blockchain-powered platforms like IBM Food Trust are already enabling companies to ensure sustainable and ethical supply chains in the food industry.

2. Decentralized Energy Systems

Blockchain is revolutionizing the energy sector by enabling decentralized energy systems. Traditional energy grids often struggle with inefficiencies and limited renewable energy integration. Blockchain-based energy platforms address these challenges by:

- Facilitating peer-to-peer (P2P) energy trading: Households with solar panels can sell excess electricity directly to neighbors without intermediaries.

- Enhancing grid efficiency: Real-time blockchain data ensures optimal energy distribution and reduces wastage.

- Promoting renewable energy adoption: Blockchain tokens can represent units of green energy, incentivizing cleaner energy use.

Projects like Power Ledger and Energy Web are leveraging blockchain to create transparent and efficient energy markets, empowering individuals and communities to participate in the renewable energy transition.

3. Driving Green Financing

Financing environmental initiatives often faces challenges such as lack of transparency, high transaction costs, and limited access to funds for small projects. Blockchain-based financial instruments offer innovative solutions:

- Green bonds: Blockchain can track how funds from green bonds are used, ensuring accountability and attracting more investors.

- Carbon credit markets: Decentralized platforms enable efficient trading of carbon credits, encouraging businesses to reduce emissions.

- Crowdfunding for sustainability projects: Blockchain reduces barriers for funding small-scale, community-led green initiatives.

UNEP emphasizes the role of blockchain in making green financing more accessible and transparent, driving global efforts toward a low-carbon economy.

Challenges and the Path Forward

While blockchain offers immense potential, its implementation in environmental sustainability is not without challenges. Concerns include:

- Energy consumption: Some blockchain systems, like Bitcoin, rely on energy-intensive proof-of-work mechanisms. Transitioning to eco-friendly alternatives like proof-of-stake is essential.

- Adoption barriers: Many industries and governments are still hesitant to embrace blockchain due to its complexity and regulatory uncertainties.

To fully realize blockchain’s potential, collaboration among governments, private sectors, and international organizations is crucial. Policies promoting sustainable blockchain practices and investments in education and infrastructure will pave the way for widespread adoption.